Oct

2024

Middle East crisis: How oil price outcomes will impact wider financial markets

DIY Investor

11 October 2024

Although the market response has so far been relatively muted, a rise in the oil price could impact inflation and lead to higher interest rates – by Malcolm Melville and David Rees

The conflict in the Middle East has witnessed an escalation in recent days. From an investment standpoint, the main question to ask in situations of heightened geopolitical risk like this is: “what is the transmission mechanism from this event to markets?” Or to put it in simpler terms, “what impact could this have on inflation, interest rates and economic growth?”

Oil prices have recently climbed to above $80 per barrel, having fallen to around $70 per barrel in early September. The recent rise suggests investors may be growing warier of the impact the conflict could have on oil supply. We spoke to Malcolm Melville, Fund Manager, Energy, and David Rees, Senior Emerging Markets Economist, to see how they think the evolving conflict could impact oil prices and the wider economy.

Malcolm Melville, Fund Manager, Energy:

“The first point to make about oil is that supply and demand dynamics are currently fairly balanced for 2025, excluding OPEC’s proposal. Lower interest rates in developed markets and recent stimulus in China may generate increased demand but the demand growth is forecast to be absorbed by small increases in production from various producers.

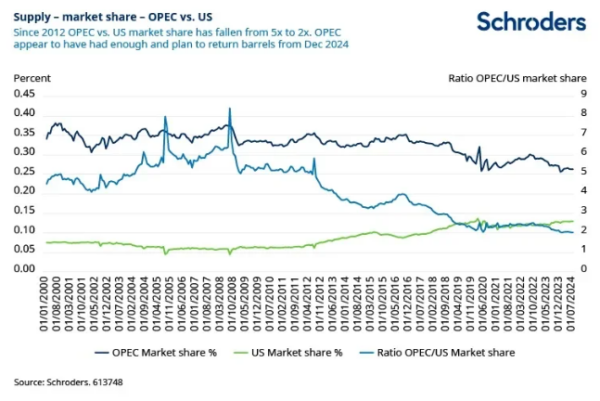

“However, OPEC has significant spare capacity after cutting supply in recent years to stabilize prices in the face of soft demand. These supply cuts have led to OPEC losing market share, notably to the US, and it is planning to return extra supply from December this year. Spare capacity from OPEC is currently very high at around five million to six million barrels of oil per day and that’s in the context of global oil demand of 102 million barrels of oil a day. That could imply a significant surplus of oil starting to emerge.

“A concern for investors is the risk that Israel may target Iran’s Kharg oil facility in the Persian Gulf. The majority of the 1.7 million barrels per day which are exported by Iran comes from the Kharg oil terminal. It is one of the largest oil terminals in the world and was targeted and damaged by Iraq during the Iran-Iraq war in the 1980s. The Kharg oil terminal is a real pinch point if Israel wanted to impact Iran’s ability to export oil. And they may argue that now is the time to do so, given OPEC’s spare capacity could offset the loss of Iranian oil.

“However, if Israel were to weaponize oil by taking out the Kharg oil terminal, that opens the possibility that Iran could retaliate and do something such as disrupting the Straits of Hormuz. Situated off the coast of Iran, the waters in the Straits are very shallow, with narrow shipping lanes of two miles wide in each direction. Around 20% of all oil flows through this strategic bottleneck.

“If Israel attacks Iran’s oil facilities on Kharg Island, the global oil price could jump to somewhere in the region of $85-$90 per barrel, which is manageable for markets and where the oil price was in April of this year. But as soon as Iran hints that they are going to do something in the Straits of Hormuz, oil prices could spike sharply higher. I don’t think it’s unrealistic to suggest that the oil price could go back to its all-time high of $147 per barrel as the market would potentially be losing 20% of its supply.

“People may question why Iran would want to close the Straits of Hormuz as it would affect its own ability to export. However, if their oil terminal has been taken offline due to military attacks by Israel, then they won’t be exporting oil anyway. And they don’t necessarily need to close the whole Straits but could launch attacks on oil tankers, delay flows and generally cast doubt on the feasibility of exporting oil via this route.

“In conclusion, there is significant OPEC spare capacity, but then there is the growing risk of a severe disruption to supply. And it’s going to be a balancing act between those two forces which is going to drive the direction of oil prices.”

David Rees, Senior Emerging Market Economist:

“It’s not our base case, but we have been modelling a “Middle East war” economic scenario for a year now. It’s a low probability, high impact scenario. When we first modelled it, we assumed it would shave a little bit off global growth.

“The main way that scenario plays out in the rest of the world is through the oil price, which would push up inflation compared to our baseline. And that scenario would see oil prices climbing well over $100 to somewhere like $150 a barrel. But so far, oil prices have struggled to crack the $80 a barrel level.

“We would need to see oil prices climb above $100 a barrel and stay there for a prolonged period of time for there to be any meaningful change in the inflation outlook or to put any pressure on central banks to change their current interest rate policy.”

Subscribe to our Insights >

![]()

Please remember that the value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

This marketing material is for professional clients or advisers only. This site is not suitable for retail clients.

Issued by Schroder Unit Trusts Limited, 1 London Wall Place, London EC2Y 5AU. Registered Number 4191730 England.

For illustrative purposes only and does not constitute a recommendation to invest in the above-mentioned security / sector / country.

Schroder Unit Trusts Limited is an authorised corporate director, authorised unit trust manager and an ISA plan manager, and is authorised and regulated by the Financial Conduct Authority.

On 17 September 2018 our remaining dual priced funds converted to single pricing and a list of the funds affected can be found in our Changes to Funds. To view historic dual prices from the launch date to 14 September 2018 click on Historic prices.

Leave a Reply

You must be logged in to post a comment.