Dec

2024

US Market Triumphant at Trump’s Return; Global Impact Still Unclear

DIY Investor

22 December 2024

With Trump’s return to office in January seemingly buoying the US market, Jason Da Silva explores why, and how, it could affect the global markets

US risk assets soared in November. Investors cheered by the election of Donald Trump bid up assets ranging from cryptocurrencies to US banks. Indiscriminate buying has broadened this year’s US equity rally from the very narrow market leadership we saw from the mega-cap tech stocks for most of the year.

Da Silva comments: “Presidential elections tend to lead to relatively muted market reactions, so why have we seen such a sharp rally this time? While Trump was favoured to win the election, a ‘red sweep’ of Republicans taking the presidency, the House, and the Senate was less likely so the market expects a much friendlier business backdrop. Taxes are likely to drop, adding an estimated 4% to US equities earnings, but more impactful will be lighter touch regulation.”

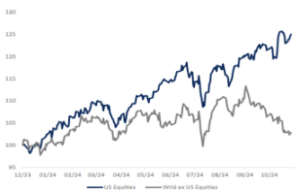

“The ‘America First’ agenda under Trump unfortunately resulted in a decline in global equities (ex-US) in Q4. Year-to-date, the S&P 500 has returned 27%; global equities (ex-US) just 7%. Trump referred to tariffs as “the most beautiful word”, but a significant trade war will have a disproportionately negative impact on China, Europe, and Asian exporting nations.”

-

US equity performance compared to non-US equities:

The tariff threat comes at a bad time for Europe. European growth has been weak since the summer as the manufacturing continues to contract (November PMIs fell to 45) – and particularly acute in Germany. While European equities are cheap, a poor growth outlook has seen reallocating capital away from Europe. We think European bonds will be well supported though, as the ECB cut rates to avoid recession.

- The global growth outlook

Da Silva continues: “Overall, the environment remains supportive for risk assets – growth remains robust, led by US exceptionalism. Following the Fed’s recent meeting, rates have been cut by a total of 125 basis points since September – easing monetary policy while growth remains above trend in the US. US growth can remain intact if Trump’s pro-business policies and tax cuts continue to buoy animal spirits across US businesses.”

While the outlook for growth outside in the US is more mixed, global equity valuations are compelling as forward price-to-earnings ratio are around average.

Furthermore, the extreme relative outperformance of US equities in the last few months is likely to not repeat to the same degree on a tactical basis. The dollar remains harder to call, while US exceptionalism is still conducive to dollar outperformance, valuations $US dollar are the most expensive in 30 years. We have limited conviction of the direction in the dollar, and remain neutral.

Fixed income assets have de-rated since September, with the US 10-year yield rising from 3.6% to 4.2% today. Given the strong growth outlook, which can lead to upside risks on inflation, we think bonds are fairly valued. We would need more convincing evidence of inflation undershooting central bank targets to significantly overweight fixed income.

Jason Da Silva is Director of Global Investment Strategy at Arbuthnot Latham

Leave a Reply

You must be logged in to post a comment.